Understanding health insurance in the United States of America (USA) can feel confusing and overwhelming. You might wonder what it really covers, how much it will cost, or why it’s so important for your well-being and finances.

This guide will clear up those questions and help you make smart choices about your health coverage. By the end, you’ll feel confident and ready to protect yourself and your loved ones without the stress. Keep reading to discover everything you need to know about health insurance in simple, clear terms.

Health Insurance Explained in the United States

How Health Insurance Works : Health insurance helps cover the cost of medical care in the United States of America (USA). It protects you from paying large bills. You pay a fee each month, called a premium. In return, your insurance helps pay for doctor visits, tests, and treatments.

What Is A Premium?

The premium is the amount you pay each month. It keeps your health insurance active. You pay it even if you do not use any health services. The premium cost can change based on your plan and age.Understanding Deductibles

The deductible is the amount you pay before insurance starts to help. For example, if your deductible is $1,000, you pay the first $1,000 of medical bills. After that, insurance covers part or all of your costs.What Are Copayments And Coinsurance?

Copayments are fixed fees you pay for doctor visits or medicine. Coinsurance is a percentage of the cost you pay after the deductible. Both lower the amount your insurance has to pay.Network Providers And Why They Matter

Insurance plans have a list of doctors and hospitals called a network. Using these providers costs less. Going outside the network usually means higher costs or no coverage.

Types Of Health Insurance Plans

Health insurance plans in the United States come in several types. Each type has unique features and rules. Understanding these types helps you choose the right plan. This section explains the main types of health insurance plans.

Hmo

HMO stands for Health Maintenance Organization. It requires you to pick a primary care doctor. This doctor coordinates all your health care. You need referrals to see specialists. HMO plans usually have lower costs but less flexibility. You must use doctors and hospitals in the HMO network.

Ppo

PPO means Preferred Provider Organization. It offers more freedom to choose doctors. You can see specialists without referrals. PPO plans have a larger network of providers. You can also see out-of-network doctors but pay more. These plans often cost more than HMOs.

Epo

EPO stands for Exclusive Provider Organization. It combines features of HMO and PPO plans. You must use network providers for care. No coverage outside the EPO network except emergencies. No need for referrals to see specialists. EPO plans balance cost and flexibility.

Pos

POS means Point of Service plan. It blends HMO and PPO features. You choose a primary care doctor like in an HMO. Referrals are needed for specialists. You can go out of network but pay higher costs. POS plans offer more choices but may cost more.

Key Insurance Terms To Know

Understanding health insurance means knowing some key terms. These words explain how your costs add up and what you pay for your care. Knowing these terms helps you pick the right plan and avoid surprises. Each term plays a role in how much money you spend on health care. Let’s break down the most important ones.

Premiums

Premiums are the amount you pay every month for your health insurance. This fee keeps your coverage active. Even if you don’t use any health services, you still pay your premium.

Deductibles

A deductible is the amount you pay for medical care before your insurance starts to help. For example, if your deductible is $1,000, you pay the first $1,000 of your care. After that, your insurance covers part of the costs.

Copayments

Copayments, or copays, are fixed amounts you pay for a service. For example, you might pay $20 for a doctor visit. The insurance covers the rest of the cost.

Coinsurance

Coinsurance means you pay a percentage of the cost after meeting your deductible. If your coinsurance is 20%, you pay 20% of the bill. The insurance pays the other 80%.

Out-of-pocket Maximum

This is the most money you pay in a year for covered services. After reaching this limit, insurance pays 100% of your costs. It protects you from very high expenses.

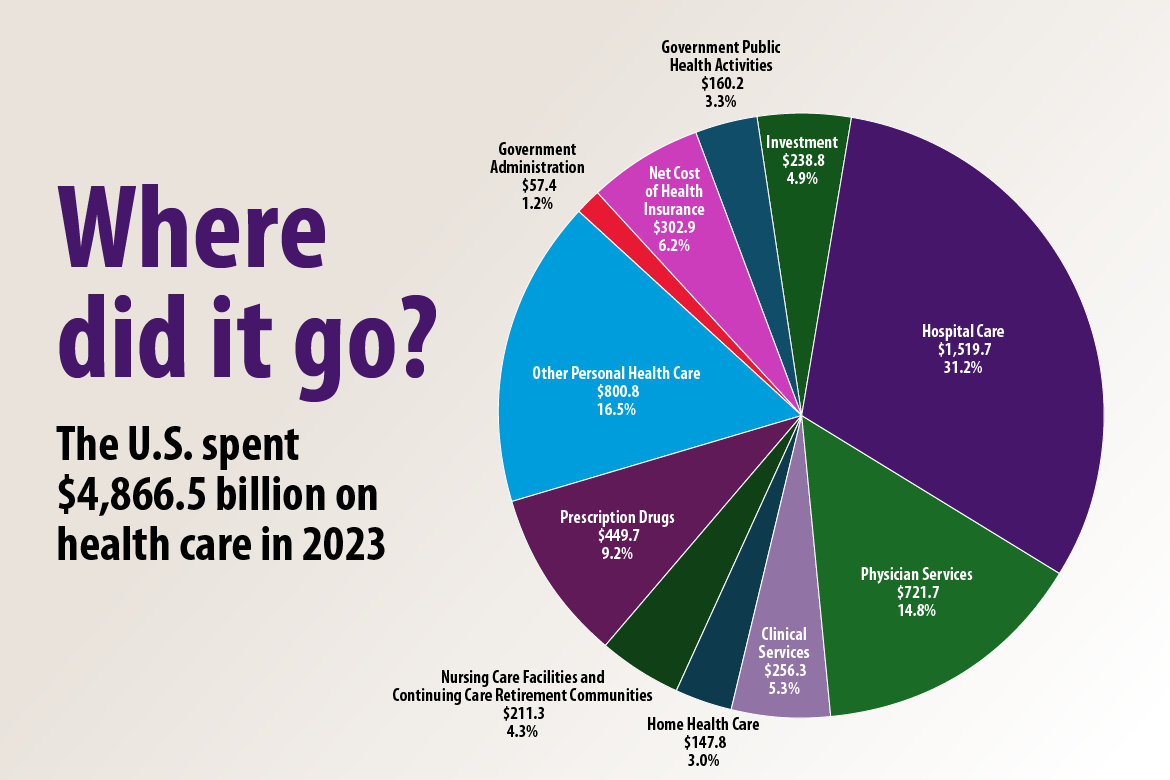

Credit: www.ama-assn.org

How To Choose The Right Plan

Choosing the right health insurance plan in the United States can feel confusing. Each plan offers different benefits, costs, and provider choices. Understanding key factors helps you pick a plan that fits your health needs and budget. Focus on what matters most to you.

Assessing Your Needs

Start by thinking about your health care needs. Do you visit doctors often? Do you need regular medicine? Consider any planned surgeries or treatments. Also, think about your family’s health needs. Knowing this helps you choose coverage that matches your situation.

Comparing Costs

Look closely at each plan’s costs. Check monthly premiums, deductibles, and copayments. Don’t forget about out-of-pocket maximums. Lower premiums might mean higher costs later. Balance what you pay monthly with what you pay when you get care.

Checking Provider Networks

Check if your doctors and hospitals are in the plan’s network. Staying in-network saves money. Out-of-network care usually costs more or may not be covered. Make sure your preferred providers are included to avoid surprise bills.

Health Insurance Marketplace

The Health Insurance Marketplace is a service that helps people buy health insurance. It offers many plans from private companies. These plans meet rules set by the government. The Marketplace shows clear information about costs and coverage. It helps people compare plans side by side. This way, choosing the right plan becomes easier. The Marketplace is open in every state. It works best for those without insurance at work or through government programs. It also helps people who want to check if they qualify for financial help. The goal is to make health insurance more affordable and accessible.

Enrollment Periods

Enrollment Periods are specific times to sign up for health insurance. The main period is called Open Enrollment. It happens once a year. Outside this time, you can only join if you qualify for Special Enrollment. This includes events like marriage, birth of a child, or loss of other coverage. Missing these periods means waiting until the next Open Enrollment.

Subsidies And Financial Assistance

The Marketplace offers subsidies to reduce insurance costs. These are based on your income and family size. Subsidies lower monthly premiums and out-of-pocket costs. Many people qualify for this help. It makes health insurance affordable for more Americans. Financial help is automatically checked when you apply.

How To Apply

You can apply online at HealthCare.gov or your state’s Marketplace site. The application asks about your income, household, and current coverage. It only takes a few minutes. After you apply, you see plans and prices that fit your situation. You can also apply by phone or with help from local agents or navigators. Choose the best plan and complete enrollment to get coverage.

Medicaid And Medicare Basics

Medicaid and Medicare are two main health insurance programs in the United States. They help millions of people get medical care. Each program serves different groups and has unique rules. Understanding these basics can help you know which program fits your needs.

Eligibility

Medicaid is for low-income individuals and families. Some states offer Medicaid to pregnant women, children, and people with disabilities. Income limits vary by state. Medicare is mainly for people aged 65 or older. It also covers younger people with certain disabilities or diseases.

Coverage Differences

Medicaid covers a wide range of services. These include doctor visits, hospital stays, and long-term care. Some states add extra benefits like dental or vision care. Medicare has different parts. Part A covers hospital care. Part B covers doctor visits. Part D helps with prescription drugs. Medicare does not cover all costs. Many use extra plans to fill gaps.

Enrollment Process

Medicaid enrollment depends on your state. You apply through your state’s health agency or online. The process can take days or weeks. Medicare enrollment starts three months before turning 65. You can sign up online, by phone, or in person. Missing the enrollment period can cause penalties.

Common Coverage Exclusions

Health insurance plans in the United States do not cover everything. Knowing what is excluded helps avoid surprises. This section explains common coverage exclusions found in many plans.

Pre-existing Conditions

Some insurance plans do not cover health problems that existed before the policy started. This means treatments for these conditions might not be paid for. It is important to check if your plan covers pre-existing conditions.

Alternative Treatments

Many plans exclude alternative treatments like acupuncture or herbal medicine. These methods are often seen as not standard or proven. Patients usually pay out-of-pocket for such therapies.

Experimental Procedures

Insurance rarely covers treatments labeled as experimental or investigational. These are new procedures not fully tested. Coverage may be denied until the treatment is widely accepted.

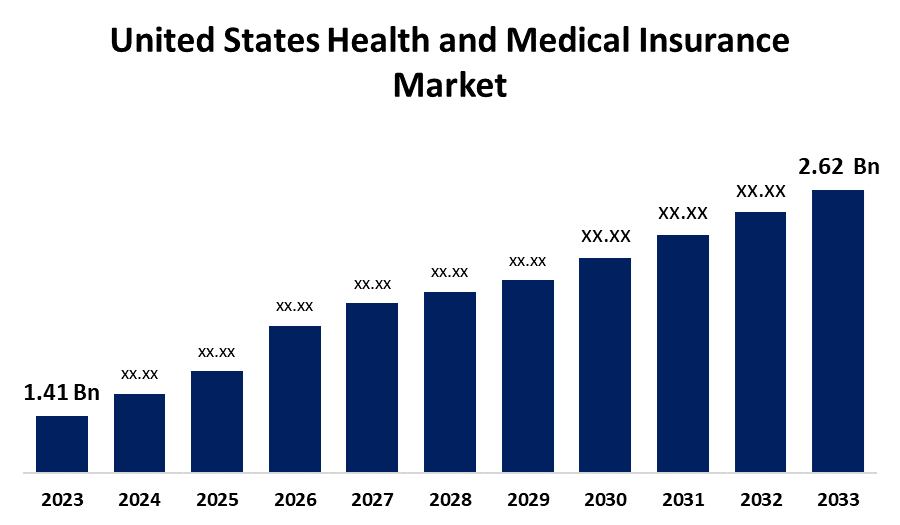

Credit: www.sphericalinsights.com

Filing Claims And Getting Reimbursements

Filing claims and getting reimbursements is a key part of using health insurance in the United States. This process helps you pay for medical bills without paying the full amount upfront. Understanding how to file claims and track your payments saves time and avoids confusion. Knowing the right steps makes the process smoother. You get money back for covered medical services. Sometimes claims get denied. Knowing how to appeal denied claims helps you get the money you deserve.

Claim Process

Start by collecting all necessary documents. These include bills, receipts, and proof of service. Fill out the claim form clearly and completely. Submit the claim to your insurance company. Many insurers allow online submissions for faster processing. Keep copies of all documents for your records. The insurance company reviews the claim carefully. They decide what part they will cover based on your policy. This step may take a few weeks.

Appealing Denied Claims

Claims may be denied for many reasons. It could be missing information or a service not covered. Review the denial letter carefully. Understand why the claim was denied. You can appeal by sending a written request. Include any new or missing information. Be polite but firm in your appeal. Insurance companies must respond within a set time. Keep all communication for your records. Persistence can often lead to a successful appeal.

Tracking Payments

After approval, the insurance company sends payment to you or your provider. Check your insurance account online for payment status. Confirm the amount matches the approved claim. Keep track of all payments received. This helps avoid errors or missed payments. Contact your insurer if payment delays or errors occur. Staying organized makes managing health insurance easier.

Tips To Lower Health Insurance Costs

Health insurance costs can be high in the United States. Many people want to lower these costs without losing coverage. Simple steps can help reduce your monthly payments and out-of-pocket expenses. Focus on smart choices that protect your health and wallet.

Using Preventive Care

Preventive care includes check-ups, vaccines, and screenings. Most insurance plans cover these services for free. Regular visits catch health problems early. This can stop costly treatments later. Staying healthy means fewer doctor visits and lower bills.

Choosing Generic Medications

Generic drugs have the same effects as brand-name drugs. They cost much less. Ask your doctor or pharmacist about generic options. Using generics saves money on prescriptions. It helps keep your insurance costs down too.

Maximizing Benefits

Know your insurance plan’s benefits well. Use all covered services to get full value. Some plans offer discounts on health programs or gym memberships. Taking advantage of these can improve your health. Better health means fewer medical costs in the future.

Credit: venturevalkyrie.com

Frequently Asked Questions

What Is Health Insurance In The United States?

Health insurance helps pay for medical costs like doctor visits and hospital stays. It reduces your out-of-pocket expenses. Many plans cover preventive care and emergencies.

How Does Health Insurance Work In The Us?

You pay a monthly premium to keep your insurance active. When you get care, the insurance pays part of the bill. You may also pay deductibles and copayments.

Who Needs Health Insurance In America?

Everyone benefits from health insurance, especially families and people with ongoing health needs. It protects against high medical bills. The law requires most adults to have coverage.

What Types Of Health Insurance Plans Exist?

Common plans include HMOs, PPOs, and EPOs. Each has different rules about doctors and hospitals you can use. Costs and coverage vary by plan type.

How To Choose The Best Health Insurance Plan?

Compare plans based on premiums, deductibles, and coverage limits. Think about your health needs and budget. Use online tools or speak with a licensed agent.

Conclusion

Understanding health insurance helps protect your well-being and finances. Choose a plan that fits your needs and budget. Keep track of coverage details and costs. Ask questions if something is unclear. Stay informed about changes in health policies. Good insurance brings peace of mind for you and your family.

Health care is easier to manage with the right plan. Take small steps to learn more and stay covered. Health insurance matters for a safer, healthier life. Meta Description: Health insurance explained in the United States covers how policies work, key benefits, and common terms to help individuals navigate healthcare coverage options.