Are you confused about life insurance in the USA? You’re not alone.

Understanding how life insurance works can feel overwhelming, but it’s one of the smartest moves you can make for your family’s future. This guide will break down everything you need to know in simple terms. By the end, you’ll feel confident about choosing the right plan that protects what matters most—your loved ones.

Keep reading, because your peace of mind starts here.

Life Insurance Explained

Types Of Life Insurance: Choosing the right life insurance means understanding the main types available. Each type has different features and benefits. Knowing these helps you pick a plan that fits your needs and budget. Here is a simple guide to the common types of life insurance in the USA.

Term Life Insurance

Term life insurance covers you for a set period, usually 10, 20, or 30 years. It pays a death benefit only if you pass away during the term. This type is often cheaper because it does not build cash value. Many people choose term life for affordable, straightforward protection.

Whole Life Insurance

Whole life insurance provides coverage for your entire life. It includes a savings element called cash value that grows over time. You can borrow against this cash value or let it grow tax-deferred. Premiums for whole life are higher but stay the same throughout your life.

Universal Life Insurance

Universal life insurance offers flexible premiums and death benefits. It also builds cash value based on interest rates. You can adjust your payments and coverage as your needs change. This type suits those who want more control over their policy and potential savings growth.

How Life Insurance Works

Life insurance provides financial security to your loved ones after you pass away. It works by offering a contract between you and an insurance company. You pay money regularly. The company pays a sum of money to your beneficiaries when you die. This helps cover expenses and supports your family.

Policy Basics

A life insurance policy is a legal agreement. You choose a coverage amount, which is the money your family will get. There are different types of policies. Term life insurance covers you for a set number of years. Whole life insurance lasts your entire life and may build cash value. The policy explains the rules, costs, and benefits.

Premiums And Payouts

Premiums are the payments you make to keep the policy active. They can be monthly, quarterly, or yearly. The amount depends on your age, health, and coverage amount. If you stop paying premiums, the policy may end. When you pass away, the insurer pays the payout, also called the death benefit. This money goes to your named beneficiaries. They can use it for bills, debts, or daily expenses.

Choosing The Right Policy

Choosing the right life insurance policy is important for financial security. It protects your loved ones in case of unexpected events. Picking a policy that fits your needs avoids wasting money or facing gaps in coverage. Focus on what matters most. Consider your family’s future, debts, and ongoing expenses. A clear view of your needs helps narrow down the best options.

Assessing Your Needs

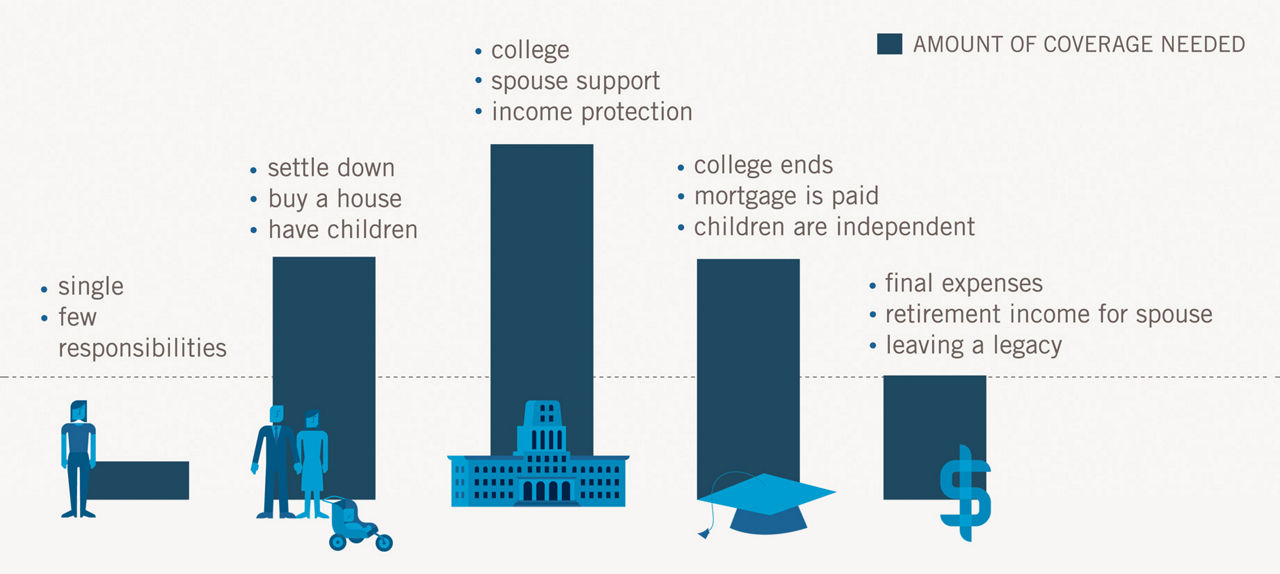

Start by listing your financial responsibilities. Think about your mortgage, daily bills, and children’s education costs. Include any debts that need to be paid off. Estimate how much money your family will need to live comfortably. Factor in future expenses like college fees or medical care. This amount guides the coverage you should buy. Also, consider how long your family will need support. Some policies cover a fixed number of years, while others last a lifetime. Choose based on your situation.

Comparing Policies

Look at different types of life insurance policies. Term life offers coverage for a set period. Whole life covers you for life and builds cash value. Check the premiums for each policy. Lower premiums might mean less coverage or shorter terms. Balance cost with protection level. Read the fine print. Understand what is covered and any exclusions. Some policies have restrictions that could affect your payout. Consider the insurer’s reputation. Choose a company with good customer service and reliable claims processing. This ensures peace of mind.

Life Insurance Benefits

Life insurance offers many benefits that protect you and your loved ones. It provides peace of mind by securing your family’s financial future. Choosing the right policy helps cover expenses and supports long-term goals. Understanding these benefits can help you make better decisions for your needs.

Financial Security

Life insurance ensures your family has money after you pass. It can cover daily living costs like rent, food, and bills. It also helps pay off debts such as mortgages or loans. This support reduces stress during difficult times. Your loved ones can focus on healing without money worries.

Tax Advantages

Life insurance policies often come with tax benefits. The death benefit is usually tax-free for your beneficiaries. Some policies allow tax-deferred growth of cash value. You may also borrow money from your policy without paying taxes. These advantages make life insurance a smart financial tool.

Common Riders And Add-ons

Life insurance policies often come with options called riders or add-ons. These extras let you customize your coverage. Riders add benefits or change terms. They help protect you and your family better. Many riders cost little but add great value.

Accidental Death

This rider pays extra money if death happens by accident. It covers cases like car crashes or falls. This helps families with unexpected losses. It usually doubles the death benefit. A small extra cost can give big peace of mind.

Waiver Of Premium

This rider stops you from paying premiums if you become disabled. It keeps your policy active during tough times. You do not lose coverage even if you cannot work. This rider protects your insurance and your budget. It is useful for long-term protection.

:max_bytes(150000):strip_icc()/WholeLifeInsurance-273c776c0b234dbbb2bbfef4f71954de.jpg)

Credit: www.investopedia.com

Application Process Tips

Applying for life insurance in the USA can feel confusing. Simple steps make the process easier and faster. Understanding what to expect helps you stay calm and prepared. Here are some important tips for the application process. They focus on medical exams and filling out forms. These tips will help you avoid common mistakes and complete your application smoothly.

Medical Exams

Most life insurance plans require a medical exam. This exam checks your health to set the right premium. The test usually includes blood pressure, blood sample, and urine test. Prepare by getting enough sleep and avoiding caffeine before the exam. Wear loose clothing for easy access to your arm. Answer the nurse’s questions honestly and clearly. Some policies offer no-exam options but expect higher costs or lower coverage. The exam results help insurers offer fair prices based on your health.

Filling Out Forms

Complete your application forms carefully and truthfully. Mistakes or missing details can delay approval. Use simple and clear language to describe your medical history. Double-check names, dates, and contact details. This avoids errors that slow down the process. If unsure about a question, ask your insurance agent or company representative. Keep copies of all documents for your records. Accurate forms speed up underwriting and help you get covered faster.

Avoiding Common Mistakes

Understanding life insurance is important. Many people make simple mistakes that reduce their coverage value. Avoiding these errors helps protect your family and financial future. Two common mistakes are underinsuring and ignoring policy reviews.

Underinsuring

Underinsuring means buying less coverage than needed. This mistake leaves your family at risk if something happens. Calculate your expenses, debts, and future needs carefully. Choose a policy that covers all essential costs. Don’t pick the cheapest option without checking if it fits your needs.

Ignoring Policy Reviews

Life changes affect your insurance needs. Ignoring policy reviews can cause gaps in coverage. Review your policy yearly or after major life events. Updates ensure your coverage matches your current situation. Keep your policy effective and useful over time.

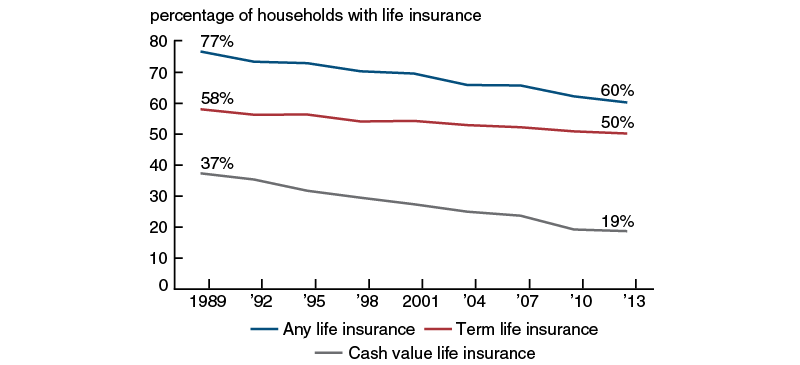

Credit: www.chicagofed.org

Credit: www.prudential.com

Frequently Asked Questions

What Is Life Insurance And How Does It Work?

Life insurance is a contract that pays money to your family after you die. You pay regular fees called premiums to keep the policy active.

Why Do People In The Usa Need Life Insurance?

Life insurance helps protect your family financially if you pass away. It can cover debts, bills, and future expenses like college.

What Are The Main Types Of Life Insurance?

The two main types are term life, which lasts for a set time, and whole life, which lasts your lifetime. Each has different costs and benefits.

How Much Life Insurance Coverage Should I Buy?

Coverage depends on your income, debts, and family needs. A common rule is 5 to 10 times your annual income.

Can I Get Life Insurance With Health Problems?

Yes, but your premiums might be higher. Some companies offer policies for people with certain health conditions.

How Do Life Insurance Premiums Get Calculated?

Premiums depend on your age, health, lifestyle, and the policy type. Younger and healthier people usually pay less.

What Happens If I Stop Paying My Life Insurance Premiums?

Your policy may lapse, meaning it ends and no money is paid. Some policies have options to keep coverage after missed payments.

How Do Beneficiaries Receive Life Insurance Money?

Beneficiaries get paid after you die by submitting a claim and death certificate. The process usually takes a few weeks.

Conclusion

Life insurance helps protect your family’s future. It offers peace of mind and financial support. Choosing the right plan depends on your needs and budget. Understanding terms and benefits makes decisions easier. This guide aims to simplify life insurance in the USA.

Start planning today to secure tomorrow.